Deep (Energy) Takes: The Future of Geothermal Energy - Part 1

Main Types of Geothermal Energy, Technical Inflections, Geothermal Learning Curves, and The Shale Revolution

Hi Deep (Tech) Takes Friends! 🧑🔬👋

So far in this very deep (energy) takes series, we’ve examined the steep learning curves shaping clean technologies, the regulatory inertia constraining U.S. energy dominance, how a potential Trump 2.0 could reshape the landscape, the evolving architecture of the grid, and the economics behind long-duration energy storage. Now, we dive even deeper—into the energy sources with the highest potential to deliver both energy abundance (a key factor in how well we compete with China) and net-zero emissions. In the next few posts, I’ll spotlight the most promising technologies shaping the future of U.S. energy production: next-generation geothermal, advanced nuclear, and hydrogen. We begin that journey by looking at geothermal energy.

Geothermal’s Overlooked Future Potential

The US is entering a new energy arms race—its most consequential since the early 2000s. As nuclear power begins to shed its contrarian image and re-enter serious policy discussions, another source of clean energy remains conspicuously overlooked: geothermal. Today, it accounts for less than 0.5% of America’s electricity generation. That figure invites skepticism. Can geothermal energy truly scale to meet 2050 climate goals? More importantly, can it address the intermittency that continues to bedevil solar and wind power, as illustrated by the now-infamous duck curve?

The answer lies not in where geothermal stands today, but in the vast energy reservoir beneath our feet. The heat stored in the Earth’s crust is estimated to hold 41 times more energy than all known petroleum and nuclear fuel reserves combined—enough to power the planet for at least a hundred generations. If next-generation drilling technologies—many adapted from the oil and gas sector—can tap even a fraction of this resource, geothermal could emerge not just as a clean energy alternative, but as a foundational pillar of grid stability. Far from marginal, it may prove to be one of the most consequential energy bets of the coming century.

Geothermal is also beginning to prove its commercial viability. Battle-tested applications are finally reaching scale, spurring a wave of market activity. Fervo Energy, a leading innovator in the space with pilot projects underway with Google and NV Energy, is reportedly preparing for an IPO next year at a valuation approaching four billion. Political momentum may be building as well. President Trump has signaled increased support for domestic energy production, and a recent emergency executive order included geothermal drilling among the technologies to be prioritized.

Which geothermal technologies are poised to reshape the energy landscape? And what breakthroughs—both technical and political—have brought us to this inflection point? As we look ahead, it's clear that geothermal is no longer a niche curiosity. Engineers, entrepreneurs, and investors increasingly see the next decade as the start of a long-overdue geothermal renaissance—one with the potential to play a critical role in addressing the climate crisis. Let’s cover the main types of geothermal and the technical inflections that helped it get this far. In our next post, we cover the policy and regulatory inflections and learn how firm, dispatchable power is geothermal’s holy grail.

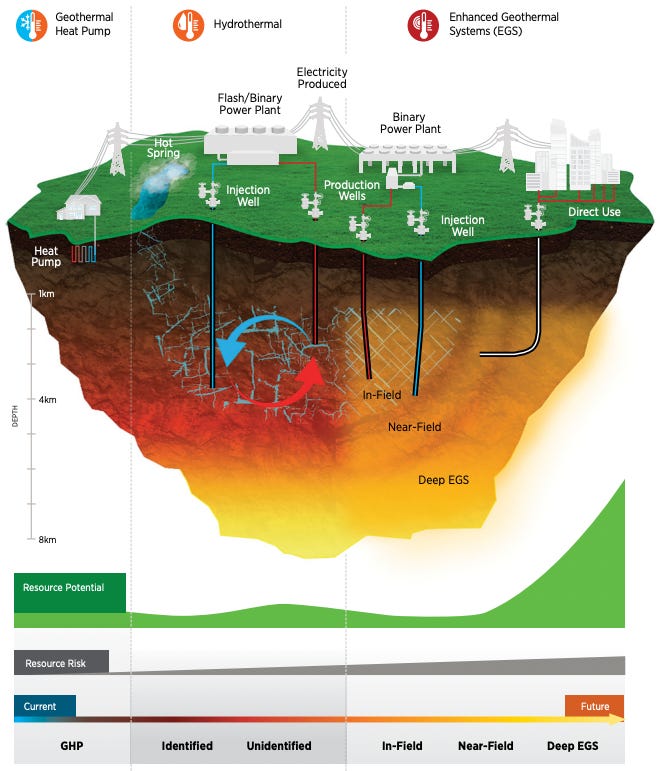

Types of Geothermal Energy: Hydrothermal Resources and Enhanced Geothermal

Geothermal, meaning “earth heat,” originates from the Earth's core, where temperatures reach approximately 6,000℃. It has provided the U.S. with reliable renewable energy since the 1890s, but its true potential lies in its ability to be an effectively unlimited energy source. The heat continuously flowing from the Earth’s interior is estimated to be around 44 terawatts (see energy intuition post if you want better intuition on energy units), which is more than twice the global primary energy consumption projected for 2025. The visible manifestations of geothermal are volcanic activity and hot springs, but also exist across various temperatures. In this post, we’ll focus exclusively on utility-scale electricity generation.

Commercial geothermal power production began in the 1960s, and since 2017, the United States has led the world in both electricity generation and installed capacity. Today, geothermal energy is produced through two primary methods: conventional hydrothermal resources and enhanced geothermal systems (EGS). In parallel, a range of advanced geothermal technologies is under active development, though none have yet reached commercial deployment.

Let’s start with conventional hydrothermal resources. Successfully establishing a hydrothermal resource requires three key elements: water, heat, and permeability. Without all three, a viable resource doesn’t exist. Access to these resources depends on the same principle that defines real estate value—location, location, location! Underground water is naturally heated and trapped in porous or fractured rock beneath an impermeable layer, forming a hydrothermal reservoir. While some of this heated water may escape to the surface as hot springs, most remains contained underground, where it can be tapped for energy production.

There is little enthusiasm for developing new hydrothermal resources due to their limited potential. Even if fully utilized, hydrothermal energy would supply only about 4% of the U.S. total generation capacity. According to the U.S. Geological Survey, identified hydrothermal resources could provide up to 9 GW of power, while undiscovered resources might add as much as 30 GW—compared to the nation’s total annual power capacity of approximately 1,100 GW. Unlocking these hidden reservoirs would require significant advancements in exploration technology. Additionally, hydrothermal resources are geographically restricted to the western U.S., Alaska, and Hawaii, with most known sites discovered due to visible surface expressions like hot springs or geysers.

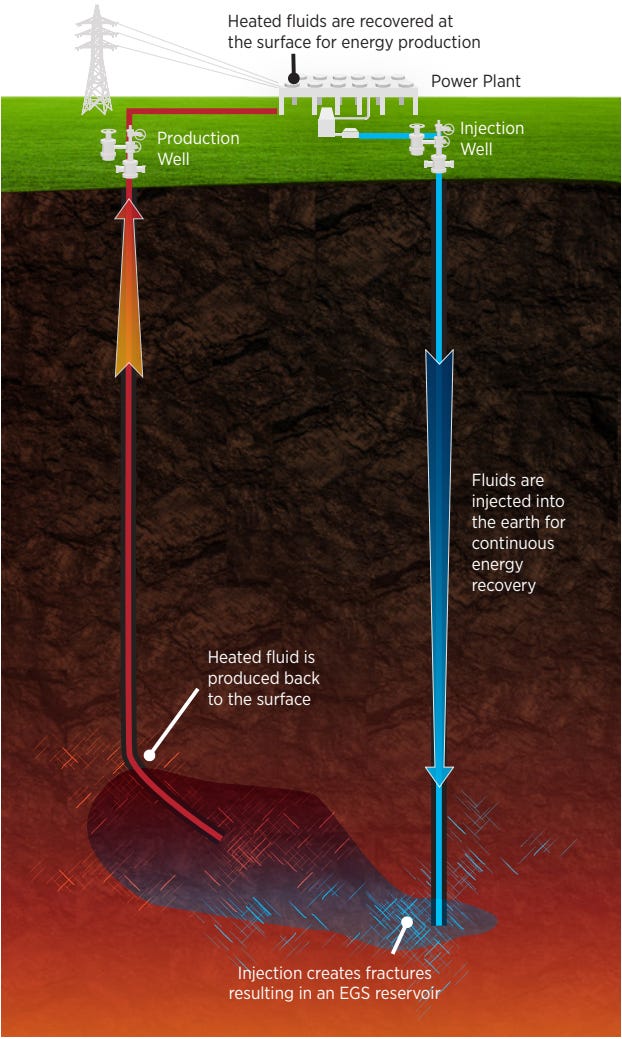

I’m far more excited about the second type of commercial geothermal energy: enhanced geothermal systems (EGS). Unlike hydrothermal resources, which require water, permeability, and heat to be viable (all three!), EGS only needs heat—and heat exists everywhere on Earth if you dig deep enough. EGS creates man-made reservoirs by injecting water into underground rock formations that lack the natural permeability needed for a hydrothermal resource. Because these reservoirs are artificially engineered, they must be carefully maintained to ensure sustained heat recovery and minimize water loss. We’ll dive into the economics of geothermal in the next section.

The U.S. Geothermal Technologies Office estimates that harnessing all theoretically viable EGS sites in the U.S. can generate up to 5,150 GW of power—five times the nation’s total installed electricity generation capacity today. In terms of heating, EGS could supply enough energy to heat all U.S. residential and commercial buildings for 8,500 years, assuming an annual consumption of 1,800 TWh for space heating.

There are multiple types of EGS because artificial reservoirs can be created at varying depths. In the near term, EGS will be deployed near existing hydrothermal resources, where it can help revive stranded or unproductive geothermal projects and turn them into energy-producing plants. This not only advances EGS technology by helping it accelerate learning through iteration (can help put geothermal on the learning curve!) but also mitigates one of the biggest risks in hydrothermal development—drilling unproductive wells.

The long-term breakthrough for geothermal lies in deep EGS, especially as subsurface engineering techniques improve to access extremely hot rock formations. At these extreme temperatures, water enters a supercritical state, carrying four to ten times more energy than liquid water. This dramatically increases the amount of heat that can be extracted from a single well, leading to significantly higher power output from a geothermal plant. Additionally, supercritical water—due to its low viscosity and high thermal conductivity—can be extracted far more efficiently. The result? Greater energy production with less fluid usage and a significantly smaller physical footprint.

Technical Inflections and Learning Curves: Riding on the Shale Revolution

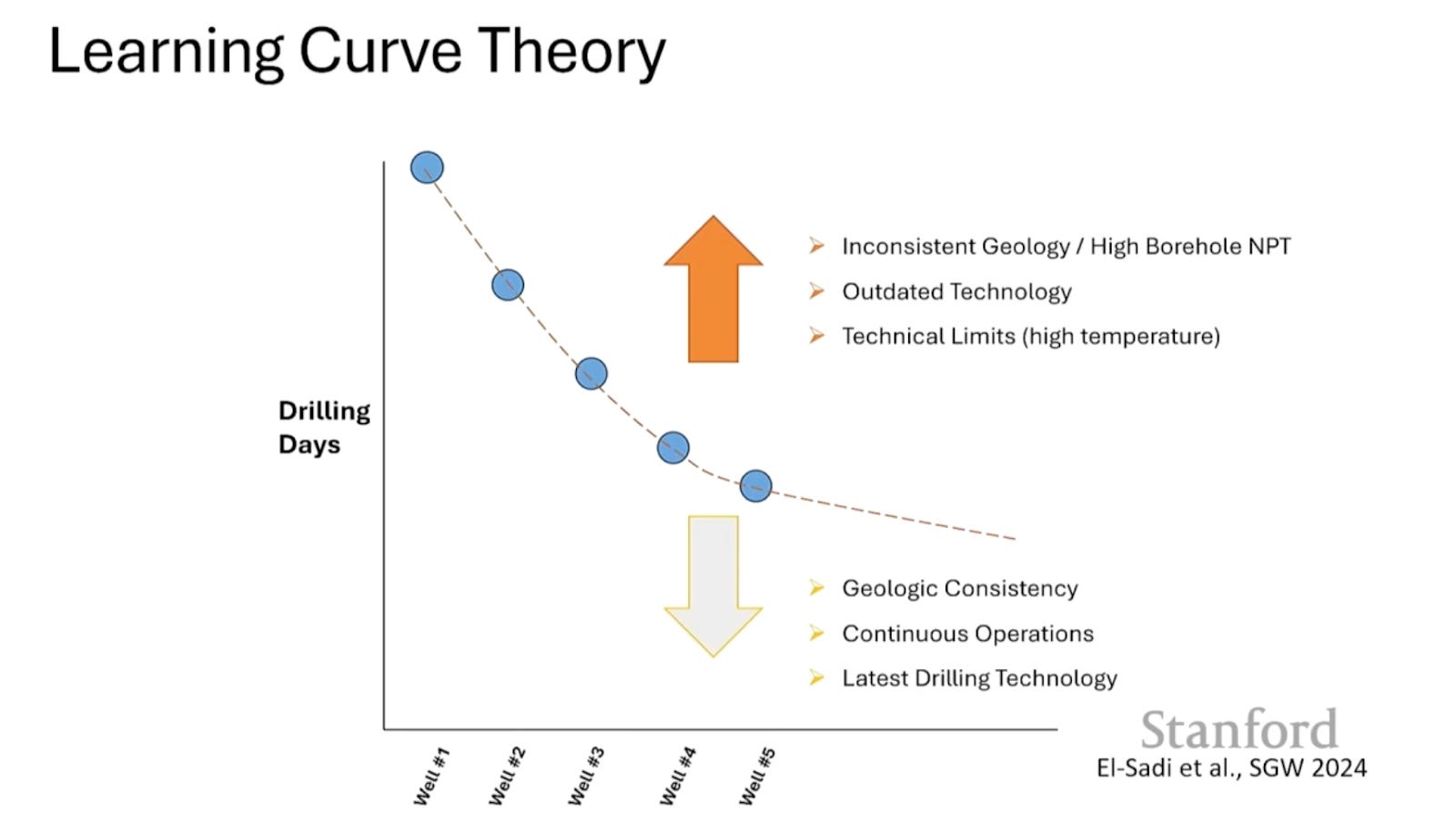

Technical, policy, and regulatory inflections are accelerating U.S. geothermal development. Let’s first explore the technical advancements, then dive into policy and regulation in the next post. The oil and gas industry has long operated at the cutting edge of drilling technology, as petroleum and natural gas become harder to extract over time. When shallow reserves are depleted, companies must drill deeper, which is why the industry hasn’t experienced the kind of learning curves seen in other technologies. Geothermal will eventually face a similar plateau when drilling advancements can no longer push deeper. But until that point, startups like Fervo Energy will continue driving progress down the cost curve.

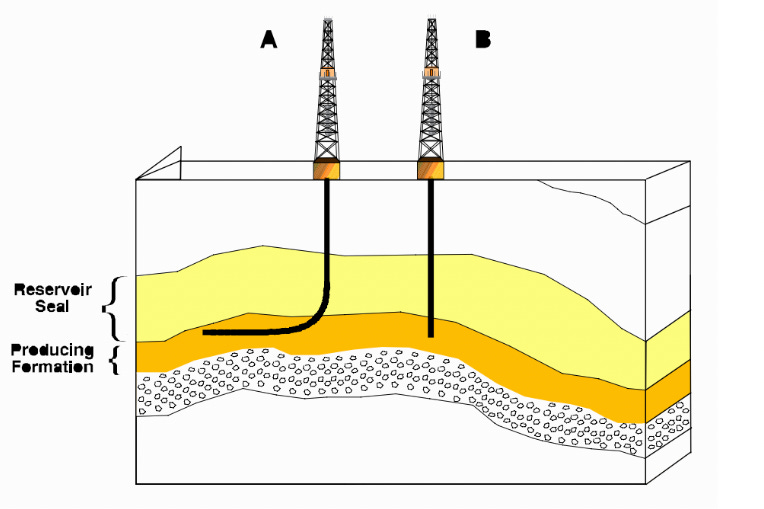

In the early 20th century, natural gas was extracted by drilling directly into a reservoir. While drillers were aware of unconventional natural gas trapped within low-permeability rock formations like shale, they lacked the technology to extract it efficiently. That changed in the 1940s when Stanolind Oil and Gas Company pioneered injecting acid into wells to widen rock pores and boost production. Over the following decades, fracking technology and fluid formulations evolved. By the 1990s, Mitchell Energy and Development Corporation refined the technique, using water mixed with proppants—sand-like particles that keep fractures open—known as slick-water fracking. This innovation unlocked vast amounts of natural gas from shale formations, transforming the energy landscape.

The next evolution of fracking combined slick-water fracking with multistage horizontal drilling. While many major gas deposits lie in rock layers less than 100 feet thick, these formations extend horizontally for miles. By drilling horizontally, wells intersect a much larger portion of the reservoir, significantly increasing oil and gas production. After acquiring Mitchell Energy and Development Corporation, Devon Energy leveraged advanced sensor technology and extensive 3D seismic data to precisely locate drillable layers.

The industry also improved efficiency by refining the extraction process. Instead of fracking an entire well at once, operators began isolating sections, fracking them individually, and repeating the process along the wellbore—a technique known as multistage fracking. Alongside these advancements, drilling technology also became more efficient. Polycrystalline Diamond Cutter (PDC) drill bits, made of synthetic diamond, replaced traditional roller-cone bits, enabling much faster drilling. Walking drilling rigs further improved efficiency by allowing rigs to move between wells without requiring full disassembly.

As of 2025, the U.S. is the world’s largest exporter of liquefied natural gas and is poised to expand its lead over the next decade. While policy decisions—such as Trump’s lifting of export limits and Biden’s push to supply Europe with an alternative to Russian gas—have played a role, technological innovation is the real driver behind this dominance. Advances in slick-water fracking, horizontal multistage drilling, improved drill bits, sensors, and 3D seismic data have steadily increased efficiency and output and geothermal startups are quick to take advantage of these battle-tested advances.

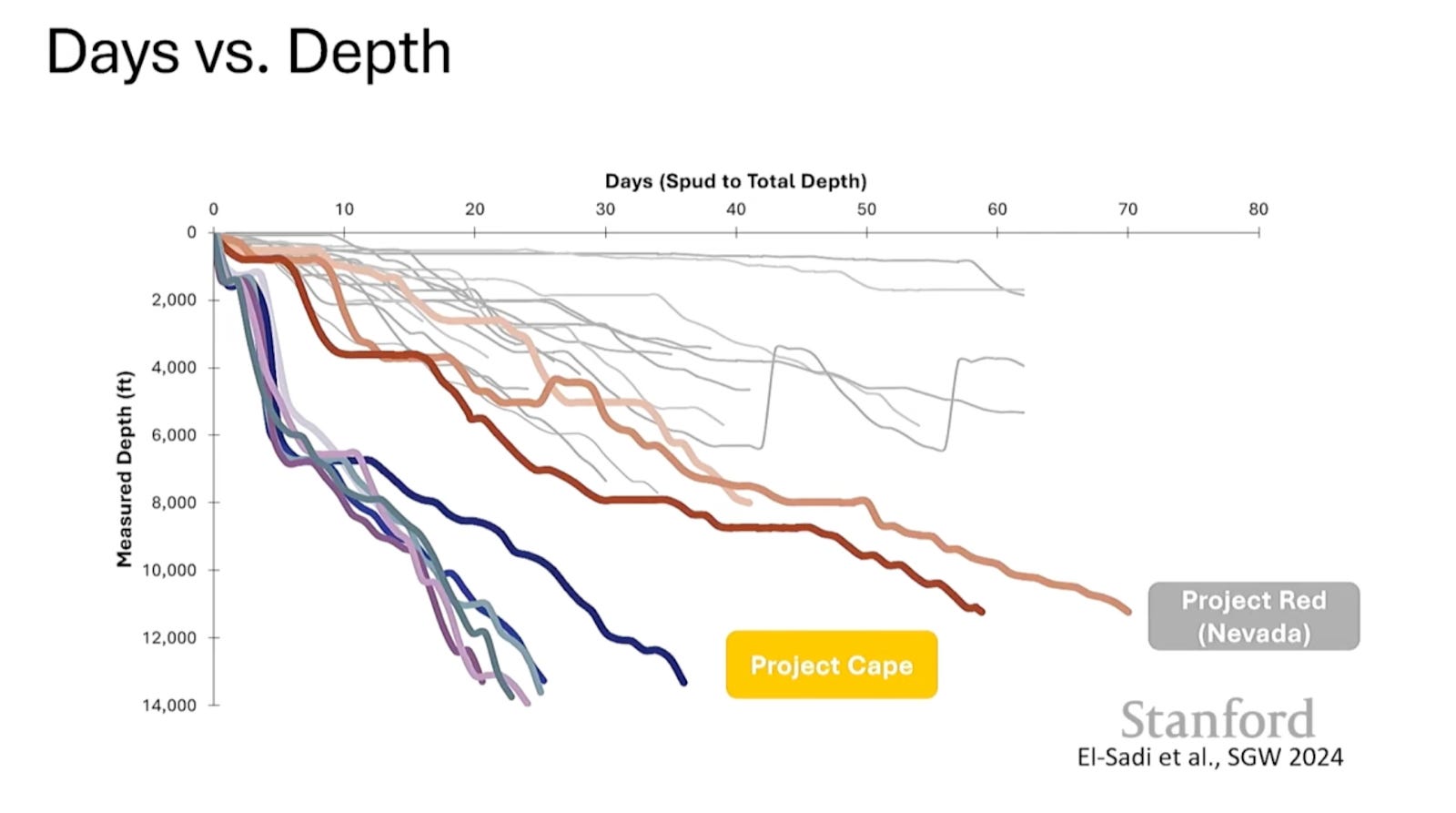

Fervo Energy is a prime example of a company leveraging the same drilling technologies and the expertise gained from shale development. In geothermal, the number of drilling days is a key factor in determining project costs and is how the industry creates its learning curve. Fervo recently completed its 30-day well test three times faster than previous attempts—effectively cutting costs by a similar margin. This is a strong step forward, but the real test lies in cutting costs even further. Despite Fervo’s progress, their pilot plant’s energy is more expensive than other renewable energy sources. Fervo’s needs to scale its success with its planned 400 MW plant, set to come online in 2028. For geothermal to become cost-competitive, these wells must continue to move down the learning curve.

Geothermal technology isn’t advancing as rapidly as semiconductors under Moore’s Law, nor is it following the steep learning curves seen in solar, wind, batteries, or electrolyzers. However, I’m still optimistic that breakthroughs in reducing drilling time will give the industry a real shot at delivering both flexible and cost-effective energy at scale. This could position geothermal as a viable competitor to other renewable sources like solar, wind, and nuclear. In my next post, I’ll discuss why geothermal energy is uniquely capable of providing firm (dispatchable) power—something no other renewable source can do as economically—and why that’s a game changer.

We’ve seen how incremental technical advancements can be just good enough to trigger massive shifts, particularly in consumer technology. Take Instagram, for example. Digital camera megapixels steadily improved until smartphone cameras became good enough for people to capture and share high-quality photos. Simultaneously, cellular networks improved to the point where users could upload those higher-resolution images quickly and seamlessly. This convergence of "good enough" innovations created an inflection point that reshaped visual communication.